Sign up for our free daily newsletter

Get the latest news and some fun stuff

in your inbox every day

Get the latest news and some fun stuff

in your inbox every day

US markets closed at record highs yesterday. The S&P 500 and Nasdaq Composite advanced as solid earnings from big names reassured investors that corporate America can still deliver, even with tariffs and trade drama swirling in the background.

In company news, PepsiCo fizzed 7.4% higher after serving up better-than-expected earnings. Elsewhere, United Airlines jumped 3.1% on a bullish outlook for the rest of the year. Lastly, Netflix slipped 1.9% in after-hours trading, even after strong results and a raised full-year forecast.

Here's the lowdown, the JSE All-share closed up 0.30%, the S&P 500 rose 0.54%, and the Nasdaq was 0.75% higher.

On Wednesday, Richemont released a decent trading update. Sales were up 6% in constant currencies, and their net cash position has grown slightly. The biggest blemish on the results was 4% drop in sales from the Asia Pacific region.

A few years ago, any drop in sales from China, Hong Kong and Macau would have seen a swift fall in the Richemont share price. Today, that is not the case, and the share price actually closed 0.9% higher. It is a testament to the hard work management has put into diversifying the group. European and American sales were up 11% and 10%, respectively, a solid showing.

Japanese sales were down 10%, but that is on the back of comparable numbers that were up 59%, so this slight drop is understandable. Japanese sales last year were driven by a weak Yen, resulting in Chinese tourists traveling to the country to take advantage of favourable pricing. The company does note that tourist sales have slowed this year, but demand from Japanese residents has remained strong, which is what you want to see.

The Specialty Watchmakers division continues to struggle, even though there was double-digit growth from the Americas. The weakness is attributed to poor sales in Asia again. This, in time, will also balance out as the group continues to diversify its product offering and regional focus. We are happy holders of this quality company.

We have an East African game ranger client who sent us a big chunk of his life savings in December 2021. The market proceeded to fall by 23% in 10 months. His portfolio was down 30% over that time. It was a terrible start.

I reached out to him a few times during this tough period and the general (delayed) response from him was as follows: "I am in the bush, clearing fire breaks and snares, I have no idea what is happening in the real world and don't really care, I trust you guys, do your thing."

Naturally, we did pretty much nothing and his account is now up nearly 60%. What is the moral of the story? Sometimes, the best investors are those who have no idea what is going on in the markets. The only noise he was listening to was the roar of a lion or the snort of a hippo, and that has worked out just fine.

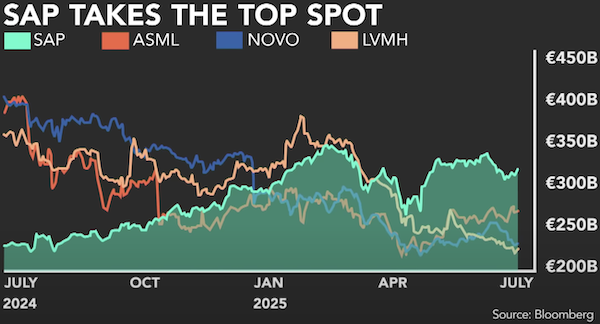

While LVMH dazzles in shop windows and Novo Nordisk dominates the weight-loss headlines, SAP has quietly climbed to a EUR322 billion market cap, cementing its place among Europe's elite. Its enterprise software runs under the hood of over 90% of Fortune 500 companies, powering everything from Coca-Cola, Apple, Walmart, to Nestle.

Born in 1972 from a group of ex-IBM engineers, SAP was built on a transformative idea: to unify company operations and process data in real time. Today, SAP's software is so deeply embedded in global business infrastructure that removing it would be akin to rewiring a plane mid-flight. That's what makes the business so sticky.

Still, that dominance hasn't gone unchallenged. Fierce rivals like Oracle, Salesforce, and Microsoft are circling. Yet the market is optimistic, SAP is priced at a lofty 40 times earnings, richer than Microsoft, Meta, or Apple. That premium reflects investors' belief that SAP will execute flawlessly from here by embracing AI, adapting to EU regulation, and fending off its many competitors. I'm not that optimistic.

Our preferred player in this space is Microsoft, by far. While SAP is deeply entrenched, Microsoft combines the breadth of cloud infrastructure (Azure), the ubiquity of Office and Teams, and fast-growing enterprise AI products like Copilot. Microsoft is also on your phone, in your browser, and behind your ChatGPT. It's diversified, dominant, and still growing fast, a rare trifecta.

AI is changing how we do things. How about using it to start a side hustle - I asked AI to build me a business and here's what happened.

Archaeologists found 5 500-year-old trapezoidal tombs. The discovery was made in Poland - Europe's first agricultural society.

Asian markets are mostly in the green this morning, riding Wall Street's positive momentum. Taiwan Semiconductor added 2.2% after delivering a record-beating quarter, proof that AI demand is still minting money.

In local company news, Redefine Properties is offloading its Rosebank Corner office block for R80 million, part of its ongoing spring clean to ditch underperforming assets and chip away at debt.

US equity futures are slightly lower pre-market. The Rand is hovering at around R17.79 to the US Dollar.

It's Friday again. Have a restful weekend.

We manage USD accounts in New York, with highly-personalised service. We've delivered industry-beating performance, thanks to low fees and good stock-picking.

Click here for more information, or email support@vestact.com.