Sign up for our free daily newsletter

Get the latest news and some fun stuff

in your inbox every day

Get the latest news and some fun stuff

in your inbox every day

On Thursday last week Alphabet (Google) released second quarter results. Revenues came in at $38.3bn, which was 2% lower than the second quarter of 2019 but 3% higher than expectations. Earnings per share smashed expectations by 28%, coming in at $10.13 a share.

As expected the advertising business took a knock. Businesses have less cash to spend on marketing and people click on fewer ads when they have less money to spend. Advertising still makes up nearly 80% of this business. Within the advertising business Youtube saw decent growth. Youtube now makes up nearly 13% of ad revenues.

What was very encouraging was the solid growth in Google cloud (sales up 42%) and Google Other, which includes Android and the app store. That was up 25% in sales.

In this environment Alphabet can be considered a value play. Unbelievable for a "FANG" stock I know. It trades on 20 times forward earnings and has over 120bn in cash. That is cheeper than the market average. They don't pay a dividend but are currently running a massive share buyback program. An extra $28bn was approved for buybacks this quarter.

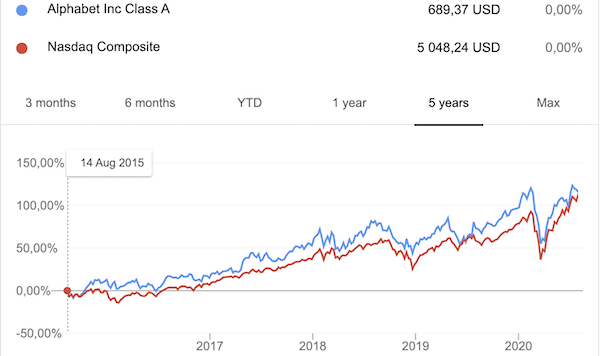

I compared the share price of Google to the Nasdaq index and the performance is very similar, see graph below. This means that Google shares have not done anything special for a while.

We see this as a really good buying opportunity. We have seen Apple and Amazon go through big patches of strong outperformance as their share prices rerate. Google is due a period of strong outperformance soon. Load up now.